The Federal Reserve has committed to pump up to $2 trillion into the system with more if needed. The European Central Bank (ECB) disappointed many in the markets by announcing €750bn with possibly more to come. The UK did its bit with £200bn too.

All this on top of what they did during the financial (credit) crisis of 2008-10.

These would be eye-watering numbers if people could actually make sense of the scale of what has been done since 2009 but they are now too big for most to comprehend.

The question is, where has all that money gone? Who has benefitted? And what purpose has it served?

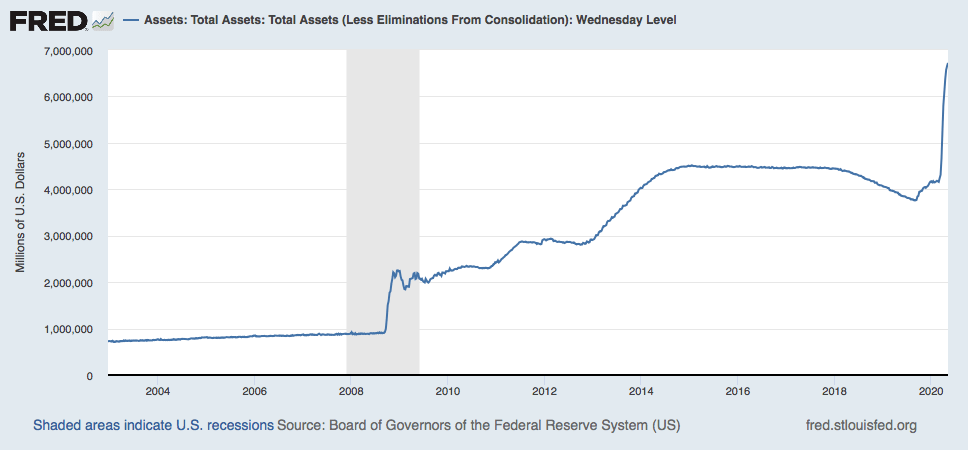

Using the US as a guide, we see central banks buying more debt to hold on their balance sheet than ever before:-

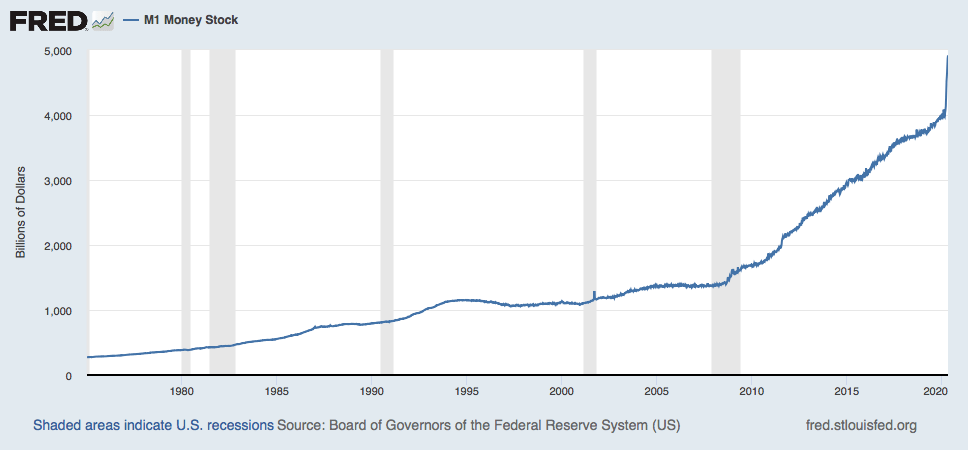

Creating more money in the system than ever before:-

Central banks buy bonds from financial institutions that were supposed to make their profits by lending it . It follows that the cheaper the cost of borrowing, the more money will be lent by the public to invest in a better tomorrow. Central banks are effectively taking debt out of the system and turning it into cash to be held in reserve whilst cutting interest rates to near zero.

Back in 2009, QE (quantitative easing) solved the astonishing reality that banks would not lend to each other because of the fear that they might not get any of it back overnight. The combination of pumping a huge amount of liquidity into the system whilst having the state take a big ownership stake of the banking sector meant those fears about banks going bust were alleviated.

This massive infusion of banking credit solved the credit crisis for the banks yet what it highlighted was that banks had now changed the way they profit.

What kind of customers do banks really want to serve?

While risking the removal of nuance in stating the obvious, it is fair to say that every tradable instrument in the financial market is priced with a spread between a slightly higher price to buy and a lower one to sell. Every trader or salesperson uses that gap between the buy and sell price ‘spread’ to profit. It really doesn’t matter how simple or complex that product is, it will be priced with a ‘spread’. Essentially, it means that trading floors make a profit simply by moving money on behalf of others irrespective of where markets are going.

The repeal of Glass-Steagall, the 1933 law that separated investment from commercial banks, led to the growth of the universal banking giants that could do everything to anybody. Banks no longer made their profit simply via lending as they could also make profits getting the investment community to buy something, anything. In 2009, Citigroup Securities and Banking generated revenues of $29.4bn from a total of $91.1bn. (See also here for separation of retail and investment banking).

QE changed the behaviour of banks in a very rational way because it just made much more sense to find as many customers in the investment community who needed to move money.

That meant that less of it has escaped into the consumer-led economy.

Bankers as a collection of people who behave rationally, just like in any other part of society.

Imagine it is your job to give out money on behalf of your employer in these COVID-19 times. From the mortgage authoriser at a local branch to the CEO, the job is always about taking a bet. Do you take a 3-year bet on a small local business that will pay a fixed/known amount of profit if they do not go bust? Or do you take a bet on the investment community that is filled with some of the most expensive minds in the world, dealing in contracts that can make a seemingly unlimited profit and be liquidated at a touch of a button?

When the economy hits hard times, lending to the small business owner becomes a much less attractive one-way bet that you are exposed to for another few years. On the trading floor of the same bank, one of those expensive minds will be able take one side of a two-way bet and, if it goes wrong, one press of a button ends that exposure.

So, if you are an employee who has the task of making safe bets on behalf of your employer, the obvious thing to do in these post COVID-19 times is to lend less to those who depend on others spending money and focus more on those who move money around searching out investments.

It is simply not prudent for those with big mortgages, huge credit card debts and expensive lives to place all that at risk for the sake of doing something different.

The consequence of this is that the transmission of QE money into the consumer economy did not happen. The most obvious place for investors to move money in a low interest rate environment remains the stock market and bonds. We have had record share prices (The NASDAQ is now worth more than every single other stock market in the world outside of the US, combined) and the normalisation of negative bond yields.

Everybody keeps talking about inflation as if it is not happening, but why does society feel so unfair?

Economic commentators have all been working hard trying to understand why all this monetary expansion has not led to inflation. Sure, consumer prices remain flat but asset inflation has been running rampant. The Bank of England estimated that an extra £28bn of extra spending was created from £375bn of QE.

We have an economy that is now dependent on the transmission of QE money based on the sheer weight of spending power at the top of society who make their profits from investing, accounting and drafting contracts to manage the movement of capital, instead of actually working to produce it. That job has been taken over by central banks around the world and the consequences of that on society have yet to fully play out. Once the public health crisis of COVID-19 is over, it might yet expose the flaws in this capital-led economy just as it has exposed the inadequacies of our public health systems that has suffered from under-investment over a decade of austerity.

Dangerous times lie ahead if the policy response remains just more of the same.

Main image: NYSE trading floor, Kevin Hutchinson, Wikimedia Commons

{kind=link}

Joe Mellon says

A friend asked if I expected inflation: I said no if by that was meant the price of a loaf of bread or a car, but yes if it meant asset prices.

My reasoning was much as Fung Wah Man’s:

– The vast pumping of money into the economy by central banks would normally cause inflation, but: these are not normal times.

For instance the furlough money has indeed been harvested from the magic money tree (invented out of thin air): most countries are vastly in debt. For the un(der)employed people who get it, it is still less than their usual wages: less demand, less inflation.

Unemployment causes recession, and low demand not inflation.

Companies are not making money, not producing goods and services and so not investing -> deflation

A lot of the bail out money went to virtual destinations: so balance sheets say the company or bank is not bankrupt, and does not need to close.

It is the virtual aspect of money: all that moved were numbers.

The last bailout to banks and companies led them to having a lot of cash and few investment possibilities.

So they bought back their own shares: stock market boom and manager bonuses.

Lots of numbers moving, but just ‘virtual’ economic activity which doesn’t affect the price of bread or a VW Golf.

What is money? It has two aspects: the virtual and the real.

A number in a bank account isnt real, nor even is a bit of paper (e.g. a €100 note).

What is real is when you walk into a store and walk out with a bag of groceries, a jacket or a car.

Inflation for those items only happens when:

– they are in short supply and/or

– normal people have a lot of loose change and are willing to spend it

But there is no shortage of goods (on the contrary – there are a lot of companies with goods they are desperate to sell), and normal people *are* short of money, and/or cautious and unwilling to spend.

So: my prediction: no inflation! (Except in asset prices for the sort of things rich people or corporations buy: e.g. stocks (shares), gold, Picassos, property in New York or London)

But multiplying the price of an asset does not make the asset more valuable in ‘real’ terms nor is it economic activity. And as Fung Wah Man points out: it is poisonous for actual economic activity: the small business, the normal person hoping to build a house, and even the person who just wants to remain employed to have enough to live.

And of course if rich people, corporations and banks have lots cash in a crisis, they will buy undervalued assets at distressed prices: concentrating wealth even more, as happened after 2008. It is reported that rich people are suffering badly, Billionaire X has ‘lost’ € 10 billion and so on (shed a neo-liberal globalized tear!). Of course the pure asset holders have lost nothing real: they still own the asset. Only if they rely on economic activity for their wealth are they in trouble: and if it gets really bad they will have to sell their asset at a firesale price to a ‘pure asset holder’ or rent seeker.

The CoVid crisis once again underlines the increasingly obvious fact: neo-liberal economics causes problems and makes many problems worse.

Bill Ramsay says

I found article and the comment useful explainers in challenging what I will call the all pervasive Thatcherite perception of what is called public debt. The Covid crisis has thrown up an opportunity for more of this.

Paul Mason , Ann Pettofor and Yannis Varoufakis are strong on this as well,

Bill Ramsay says

Please pardon my return but around the 45 minute mark of Channel 4 News Thursday 4th June a ten minute debate between conservative historian Nail Ferguson and economist , and Stephanie Kelton on the “debt myth”,

David Gow says

yes, saw it..