This post summarises the current position on grants and loans for full-time students in higher education in Scotland, and the background to it.

Background

(i) Fees and other payments

The Scottish Government funds the whole tuition cost for almost all first-time, full-time Scottish and EU students in Scotland, from the government’s cash budget. Therefore no-one from any background has to borrow for part or all of their fees. Scottish students will only need a fee loan (as students in other parts of the UK get, to defer fee payments) if they go to study elsewhere in the UK.

Between 2001 and 2006, young students entering degree-level HE full-time were liable to pay the graduate endowment, a single payment of £2,000 at 2001-01 prices, after finishing university. The income from the GE was in theory ring-fenced for student bursaries. Graduates could either pay it in cash or add the liability to their existing student loan (or take out a first-ever loan) to defer the payment. Because of exemptions for HNC/D students, including those on “2+2” models, mature students, disabled students and single parents, slightly under half of all the full-time students the SG supported were liable to pay the GE, which was bringing in around £23m p.a. by 2007 (more here). When the current Scottish Government says it brought in free tuition, it is referring to its abolition of the endowment in 2007. It is also often, in practice, describing its decision not to use devolved powers to copy either of the fee regimes which have applied in England since 2007.

(ii) Living cost grants

Scotland has relatively low student maintenance grants (here called bursaries). Most living cost support is offered instead as student loan.

Between 2010 and 2012 inclusive, the means-tested grant for younger students, Young Student Bursary, was frozen in cash terms (see here for more on how its value changed from 2001 onwards). In 2013, the Scottish Government cut its total spending on maintenance grants by around £35m, or one-third. The maximum YSB was reduced from £2,640 to £1,750, and it was withdrawn more quickly as income rose. The government lowered the income at which maximum YSB was payable from £19,300 to £16,999. Many students lost £900 a year and some much more. The Scottish Government argued they could make up the difference by borrowing to fill the gap. Older students get the lower-rate Independent Student Bursary. This was introduced as a lower-rate grant by the Scottish Government in 2010, and then also scaled back in 2013.

In 2015, the Scottish Government added £125 back on to some grants, costing it around £5m, and in 2016 it reversed most of the cut to the threshold for maximum grant, raising it to £18,999 (likely to have cost it a bit under £2m a year).

The current system

The resulting living cost model in 2016-17 is in the table below:

A particular feature of this model is that it is built round those from the lowest incomes, especially mature students, taking out the highest loans. Until grants were abolished in England in 2016, Scotland was the only part of the UK taking this approach. It means that someone at a low income who wishes to take out their full entitlement to living cost support over four years faces a debt of £23,000 plus interest if they are younger, and £27,000 plus interest if they are older. Grants are higher in Wales and Northern Ireland (where students also only have to borrow for the first £3,900 of their fees: true for Welsh students anywhere in the UK, for NI ones in NI).

Actual borrowing

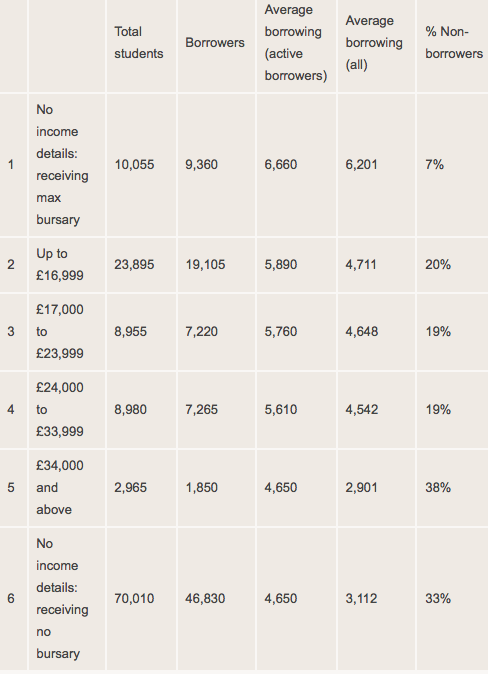

Figures on annual borrowing by income are published annually by the Student Awards Agency Scotland (SAAS). The latest are here (see Table A6). They show that Scottish students borrowed a total of £0.5bn in 2015-16.

Around 70% of Scottish students take out a loan in any given year, and almost all those who borrow, borrow the whole amount they can.

The table below is adapted from the official statistics. I’ve added two columns. One shows average borrowing across the group as a whole, i.e. including borrowers and non-borrowers. The other shows the percentage who don’t borrow in each income group. It’s reasonable to assume from other research that there are more non-borrowers in the higher income group because students’ access to family resources tends to rise as family income increases. It is likely that even within this group, non-borrowers are more prevalent at higher incomes: it is quite plausible that at, say £60,000+, non-borrowers are in the majority.

The net effect of lower income students having higher loan amounts and making more use of loans is that students in the highest income range borrowed in practice around half as much per head (around £3,000) as those in the lowest income band (over £6,000). Another way to look at this is that Groups 1 to 4 below accounted for only 43% of all students, but took out 54% of all debt.

Borrowing by income band 2015-16

Note: I’ve removed EU students (14,705) from the figure for total students, as these students can’t borrow. I have assumed that they were contained in Group 6, as very few can claim means-tested support. That may not be exactly right, but it should be near enough. Most students with an income over £34,000 will be in Group 6, which covers those who chose not to submit income details, generally because they are above the threshold for bursary. Group 1 by contrast will be those who had no relevant income to declare and got the highest bursary level. Group 5 is a small group whose income details SAAS knows, although they are over the bursary threshold. I have excluded here a very small group of low-income students separately shown in the SAAS table who anomalously have no income but don’t get full bursary: there’s something odd going on with this group (it may be that many don’t complete a full year).

Caution: final borrowing

Separate figures are published each year for students’ final borrowing. The most recent Scottish figure is £10,500. These figures are widely quoted but have to be handled with care. The average will be brought down by the large number of students in Scotland on one or two year courses, and – as shown above – any average will conceal variation by income. More on that here.

Conclusion

The Scottish system is not debt-free in the absence of fees: indeed Scottish students are borrowing a substantial amount as a group each year. The Scottish approach relies heavily on loans to cover the state’s role in providing low-income students, in particular, with living cost support. Grants are now so low that those from the lowest incomes are taking on the most of that living cost debt. Equally, at high incomes, many students will be borrowing nothing.

Defending existing policy in Scotland means defending this outcome.

First published on the author’s site CC BY-SA 4.0

Leave a Reply