The best that can be said for the Scottish Government’s new economic paper for Scottish independence, Building a New Scotland: A stronger economy…, is that it does not include some of the more hideous ideas contained within the Growth Commission report. That was the 2018 publication commissioned by the SNP and led by corporate lobbyist and former SNP MSP Andrew Wilson, which this new paper essentially supplants.

There is no talk about a core aim of doubling GDP in 15 years. All reference to a public debt ceiling of 50% of GDP and deficit reduction as the priority in the first years of independence is gone. Also missing is any reference to Scottish financial regulation “mirroring” that of the UK, and corporate tax rates being pegged to those of the UK. Faux-pax, like Scotland paying into the UK foreign aid budget rather than having its own international development policy, are missing.

However, the new paper doesn’t replace these Growth Commission policies with others. Instead, there is a blank space in their place. It’s like civil servants have gone through the Wilson Report and put red ink over anything that is obviously a hostage-to-fortune politically, saying: ‘just re-write the rest’. Plus, they have added in blue boxes with some well-meaning but fairly tepid critiques of “trickle-down economics” and references to “new economic thinking” of the “wellbeing economy” variety. Depending on your perspective, this could be considered either a savvier or a more evasive version of the Growth Commission. Even if you consider it to be politically savvy, the substance that is contained in this paper is not at all good, or even adequate.

Because although the Scottish Government’s (SG) economic plan is likely to run into less obvious problems politically than its predecessor, the financial architecture it proposes – to use the UK Pound informally, a policy widely known as ‘sterlingisation’ – is still fundamentally the same. So, it would equally land an independent Scotland in major economic problems, probably sooner rather than later. Given how financially unstable the UK and indeed world economy is, it would not be long before an independent Scotland’s finance minister would be faced with impossible choices between the interests of its creditors and the interests of the Scottish people, an invidious position that would be extremely difficult to get out of, since – as we shall see – transitioning out of Sterlingisation would be no easy task.

To understand this, we first need to grasp the structural vulnerability inherent to being an independent state without monetary powers:

In part 1, I explore a recent paper on the vulnerabilities of sterlingisation to highlight what the key problems would be.

In Part 2, I look at how transition to a Scottish currency on the basis proposed in this paper would be extremely difficult.

In Part 3, I briefly examine the case of dollarised Ecuador, and how an attempt to escape dollarisation in that Latin American nation never got off the ground.

Finally, in Part 4, I look at what the disastrous UK Government ‘mini-budget’ should and shouldn’t teach us about monetary policy, fiscal policy and financial markets.

Part 1: What’s wrong with sterlingisation?

The currency policy proposed in ‘Building a New Scotland’ is that “on independence, Scotland would continue to use the pound sterling for a period before moving to our policy of adopting a Scottish pound”. In other words, after the transition period has ended, the first independent SG would start life sterlingised: using the currency of another sovereign state. An independent Scotland would be a currency user, while the rest of UK (rUK) through the Bank of England would be a currency issuer, with no remit to consider the needs of the Scottish economy at all. Scotland would be in the monetary position of just a handful of independent states in the world: Ecuador and Panama, which are dollarised, and Liechtenstein and Montenegro, which are euroised.

University of Edinburgh Professor Iain Hardie published a paper for the Centre for Constitutional Change on an independent Scotland’s currency options at the beginning of October which is the most up-to-date academic assessment of the issue, taking into account not only monetary policy responses to the 2020 pandemic but also the 28th September Bank of England intervention to stabilise UK Government bond rates (‘Gilts’) as part of the fallout from ex-Prime Minister Liz Truss’ disastrous ‘mini-budget’. Hardie is a former investment banker and an expert on government bond markets.

Hardie’s paper is a systematic critique of sterlingisation (which he calls “informal currency union”), concluding without any room for doubt that it is by far the worst possible monetary option for an independent Scotland and a Scottish currency is “the only viable option”. On what basis does he come to this conclusion? Three main points are made:

1. The need for a “Buyer of Last Resort”

Central banking has changed. Whereas in the 1990s, when Gordon Brown made the Bank of England independent, central banking was seen as light-touch and primarily about price stability, the intrinsic vulnerability of a financialised global economy means central banks have become interventionist in order to maintain financial stability.

The Bank of England is a case in point. The use of money creation through Quantitative Easing (QE), first in 2008 to prop up the private banking sector, then in 2020 to fund massive government borrowing to respond to the pandemic crisis, and finally in September 2022 to stabilise Gilt rates and protect pension funds from a potential collapse, is all evidence of a “fundamental change”, according to Hardie, in how the BoE operates as its balance sheet continues to grow, with over £900 billion in new money created through BoE QE since 2009.

This in turn makes central banks increasingly pivotal to the fiscal policies of governments, to the extent that “without the Bank of England’s ability to create money to buy UK government debt, there could not have been the scale of COVID response that we saw,” Hardie finds. He adds that for an independent Scottish Government to have intervened on the scale of the Treasury in 2020 (most prominently through the furlough policy) without a currency-issuing Central Bank “would at best be extremely challenging, and at worst impossible.”

The reason why is because without a “Buyer of Last Resort” – a Central Bank which can fund government borrowing by creating new money – the government can only borrow from financial markets. This can become a major problem, especially in a crisis, if those financial markets don’t want to buy government bonds or demand too high a price. Crucially, knowledge of the fact that the central bank can always step in and create new money to buy government bonds has a disciplining effect on financial markets, since they know that any attempt to force up the price government must pay to borrow can be resisted through central bank intervention. Or as Hardie puts it: “Any investor considering a short position in the bonds of a government able to create its own currency must factor in the central bank reversing market weakness.” Under conditions of sterlingisation, the shoe is on the other foot: financial markets would charge the SG a premium in the knowledge that it has nowhere else to turn.

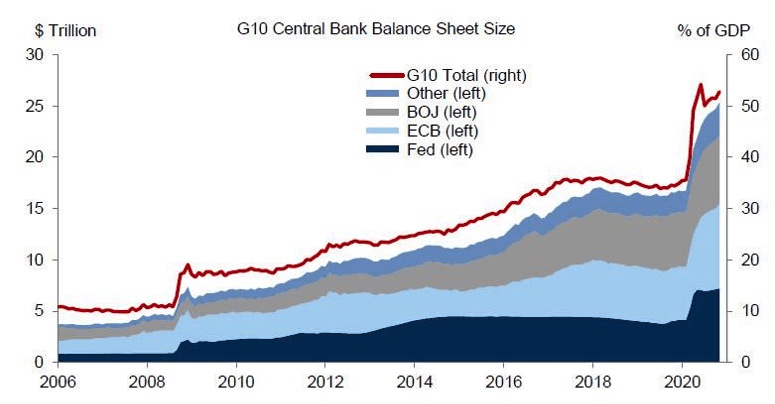

As the graph above shows, the Bank of England is by no means an outlier amongst major central banks in its use of QE in recent years. In fact, it has been on the “conservative” side, according to Hardie. This is a major and permanent feature of how central banking now works in the global economy, yet remarkably the ‘Building a New Scotland’ paper does not mention QE once, as if the SG is either unaware of its existence or is in denial about its relevance. This is a massive and unjustifiable oversight for what is an official government document (even the Growth Commission report briefly mentioned QE).

2) The risk of financial crisis

It logically follows that if an independent SG would struggle to take interventionist policies such as furlough during the pandemic crisis or the huge government borrowing now taking place to offset energy price rises, it would also struggle to cope with a financial crisis in which Scottish corporations are threatened with collapse, as in 2008 or 2020.

The means by which a monetarily sovereign central bank acts as a financial backstop to the private sector is called ‘Lender of Last Resort’ (LOLR) and, while the “Building a New Scotland” paper states that a sterlingised Scottish Central Bank would have a LOLR facility and could “ensure that deposit guarantees are in place”, there is no explanation given for how this would work. In reality, these are words devoid of their proper meaning: all a sterlingised Scottish Central Bank could do would be to borrow from financial markets, which given a broader financial crisis would be very expensive indeed, since there would be obvious questions about the scale of borrowing required and the ability of a non-sovereign country to pay. It’s at this point that a financial crisis can become a sovereign debt crisis.

Indeed, Hardie finds that an independent SG relying on private borrowing would not be feasible at all as a crisis response.

“Scotland’s ability to borrow in a crisis, and therefore for the government to respond fully to that crisis, could depend on the Bank of England deciding that the Scottish government’s ability to borrow was sufficiently core to the monetary and financial stability of the rUK to justify intervention,” he writes. “It is as easy to construct scenarios in which that would not be the case as it is to construct scenarios when it would.”

If the thought of an independent Scotland having to turn to the BoE for help does not fill you with sufficient dread, Hardie raises the prospect of an “IMF bailout” as the country’s next best option, and we all know the horror stories from Greece to Argentina of the cost of IMF ‘structural adjustment programmes’. Indeed, euroised Montenegro received an IMF bailout in June 2020 as the country’s government borrowing costs soared during the pandemic crisis.

As Angus Armstrong and Monique Ebell wrote for the National Institute of Economic and Social Research all the way back in 2013 on the risks of sterlingisation, the impact of financial and sovereign debt crises “far outweigh any marginal effect on trade” from reduced transaction costs, one of the main benefits of remaining in the sterling zone.

Armstrong and Ebell add: “There have been 218 currency crises between 1970 and 2011, 65 of which coincided with sovereign debt crises. The costs of the instability are an order of magnitude larger than the gains from increased trade.”

We live in an increasingly insecure world, not just financially but also ecologically, militarily and socially. If you don’t think that a crisis from any of these sources could strike at any time and have a profound effect on the financial system, you’ve not been paying attention. Given this context, the prospect of an independent Scotland starting life without the protections of a monetarily sovereign country is incredibly naive.

3) Additional government borrowing costs

Finally, the day-to-day additional costs of government borrowing under a sterlingised scenario are likely to be significant, and thus will increase the amount of tax revenue which ends up in the hands of private bond investors and reduce the amount which is spent on public services.

The Standard & Poor credit rating agency marked down Montenegro due to its “lack of monetary flexibility” while it marked up the Czech Republic, which has had its own currency since 1993, for its “high degree of monetary flexibility”. A 2021 study cited by Hardie found that QE saved the UK a full 1 per cent of its borrowing costs, or £12bn in 2019-20 alone. Hardie finds that the cost of borrowing under sterlingisation would be 0.5% more expensive than in a currency union, a not inconsiderable sum.

It is more difficult to compare the cost of borrowing under sterlingisation with a prospective Scottish currency, but the Czech Republic provides some basis for comparison.

“The Czech Republic is now rated the same as the UK in local currency, and its borrowing costs…have been below Gilts…The performance of its currency against the euro similarly suggests investor confidence was established relatively quickly,” Hardie finds.

Indeed, the Czech Koruna has “been generally trending upwards against the euro” since the latter currency was launched in 1999. There is little to be afraid of from a Scottish currency.

Part 2) Why the transition would not be “practicable”

‘Building a New Scotland’ promises that sterlingisation would be for an (undefined) short period, before the transition to a Scottish currency “as soon as practicable”. However, what is “soon” and what is “practicable” are likely to be very different here. In reality, such a transition would be extremely difficult to achieve in the way the Scottish Government’s economic paper proposes, due to three inter-related factors.

1.The risk of a speculative attack

Because a sterlingised Scotland would not be underpinned by a currency-issuing central bank, any transition – or even the signal towards a transition – could be in danger of leading to a shorting of SG bonds by the financial markets if they do not deem the move to be favourable to their interests. The latter reaction is likely since a Scottish currency would mean higher financial transaction costs and the duplication of banking services on both sides of the border. And to be fair to the bankers, if you are looking for safe returns why put your money into government bonds not under-pinned by a currency-issuing bank when there are many other nation-states in the world, the vast majority of which are monetarily sovereign? A potential speculative attack would be driven by hard business logic.

Such a shorting of Scottish bonds, or even its possibility, could have a chilling effect on an independent SG, as the short-to-medium term pain of a major hike in the cost of public borrowing may not be seen as worth enduring. It’s also necessary to factor in the response from the Bank of England and the UK Treasury to such a move in Edinburgh, as displeasure from London could be an added ingredient to rattle Scottish bond investors. Being caught between the hammer of the financial markets and the anvil of the Bank of England would leave Edinburgh with little wriggle room.

If you are in any doubt as to the risks involved if a sterlingised Scotland’s finance minister pursued a policy fundamentally at odds with the country’s bond investors, a 2014 Scottish Parliament Information Centre (SPICe) briefing found that sterlingisation would require “integration” with rUK “politically and institutionally” in order to maintain market confidence. SPICe suggested this would include a “single monetary policy; similar business cycles; aligned fiscal policy; aligned legislation on labour, private property, contracts, etc; single/aligned foreign policies.”

Even if a sterlingised Scotland were to somehow avoid that level of integration, it’s crucial to understand that the constant looming threat of a financial crisis or a speculative attack would have a disciplining effect on any finance minister in Edinburgh, who would have to constantly demonstrate credibility with the financial markets, i.e. following their ideological diktats. And indeed, ‘Building a New Scotland’ finds that one of the “requirements” for giving the Scottish pound a green light would be “market confidence and credibility in the macroeconomic framework”. This would only be tested when the plans are at least floated, and presumably a negative market reaction would be reason enough for an independent Scottish Government to pull back.

2.The need to accumulate foreign exchange reserves (FER)

To defend a Scottish currency on foreign exchange markets, it would be necessary to have substantial reserves. On FER, the ‘Building a New Scotland’ paper is somewhat evasive. It states: “An independent Scotland’s starting level of reserves would be for negotiation with the Westminster Government. Scotland’s population share of the UK’s foreign exchange gross reserves of $171 billion would be around $14 billion. Borrowing would be used to secure additional reserves.”

This provides little clarity on how much FER would be accumulated through debt and asset negotiations, but since it states that “borrowing would be used to secure additional reserves”, we can assume that not all, and probably not most, of the FER would be secured during the transition to independence. If we assume the paper’s figure of $14bn is more or less reasonable, let’s say that during debt and asset negotiations Scotland secured $4bn in FER. That leaves $10bn (at current exchange rates, £8.6bn) to be raised through borrowing on the financial markets. And, again, according to the paper, all of that money has to be raised in advance of the shift to a Scottish currency, since one of the three criteria of such a shift is “that foreign exchange reserves and sterling reserves are sufficient”.

To put £8.6bn in perspective, it’s more than double what the SG spends on Education and Skills in 2022/23. Or to look at it another way, it is almost half of the Scottish Government’s proposed ‘Building a new Scotland fund’, which would use £20bn of oil revenues for public investment over ten years following independence. In short, it’s not pocket change. A Scottish Government would have to convince the Scottish people that it’s worth borrowing £8.6bn to spend on FER rather than on public services or reducing taxes.

Scotland has an ageing population with growing pressure for above-inflation increases in public spending in areas like health and social care. If the case for an independent Scotland is to be won, it will be won with an anti-austerity pitch; there will be an expectation that an independent Scottish Government focuses on the immediate tasks in front of it. Any government promising to borrow £8.6bn for FER (or even £5bn for that matter) is in for a hard sell.

But the public would not be the biggest problem here. The bigger problem would be the financial markets to which, as explained above, a sterlingised Scotland would be in hawk and which are unlikely to look favourably upon such a policy – along with the Scottish Government’s own commitment to “fiscal rules”.

3. Fiscal restrictions

The vague reference to “fiscal rules” in the paper is politically expedient because a figure on these fiscal rules, as the Growth Commission gave, would immediately associate independence with austerity. (Extremely high oil prices mean that a prospective independent Scotland may currently operate a fiscal surplus, but we can expect that to change relatively quickly, and in any case the paper commits to putting all tax revenues from North Sea oil into the ‘Building a New Scotland fund’, i.e. separate from general revenue.)

Nonetheless, the paper’s clear implication is that fiscal rules would be whatever the EU settles on following the pandemic, since the paper rightly points out that the EU “Stability and Growth Pact” – which sets a limit of a budget deficit of 3% of GDP – is “currently suspended to allow member states to respond to the impact of COVID-19 and ongoing geo-political challenges”. Those rules are due to come back into force at the end of 2023 unless the EU can agree to a new reform, which is likely to be blocked by fiscal hawks like the German Finance Minister Christian Lindner. The arbitrary and economically illiterate 3% of GDP limit may not be disappearing for good.

But even if the SG fiscal rules ended up being set at, say, 5% of GDP, the £8.6bn on FER, if it were to be raised in one financial year, could only be achieved via drastic cuts elsewhere, big tax rises or a rate of economic growth not seen for decades. The last option is economically implausible while the first two are politically implausible (indeed, the paper doesn’t even mention tax powers once, a massive oversight of what would be a hugely important economic lever to re-balance the Scottish economy following independence). And remember, ‘Building a New Scotland’s’ own criteria for moving to a Scottish currency include “that Scotland is fiscally sustainable”.

One possible alternative would be to put small sums towards FER each year, say over 10 years, until it has accumulated the £8.6bn. But “as soon as practicable” in this context would mean more or less “a generation”, and a change of government could easily see the plans rolled back or the money spent on something else altogether. Meanwhile, Scotland would be living perilously as a country without monetary sovereignty. Whichever way you look at it, the currency transition would be complex and painful and as such, might not happen, even if the Scottish Government wanted it too.

Part 3: Ecuador: A case study in “monetary suicide”

We do have an example to draw on of a dollarised country where the government wanted to switch to its own currency but didn’t feel able to do so because the transition would be too difficult: Ecuador.

The north-west Latin American nation dollarised in 2000 in response to a banking crisis. In 2007, left-wing economist Rafael Correa was elected President. Correa was initially successful in his growth and redistribution policies despite operating with the dollar, but when the oil price fell in 2014, unlike its neighbours the oil-exporting nation could not devalue its currency, and the president estimated that use of the dollar cost Ecuador the equivalent of 7.4% of GDP in 2015.

“Very few countries in the world have committed a monetary suicide like Ecuador, adopting a foreign currency that behaves exactly in the opposite way we want it to,” Correa said. “Colombia devalued, Peru devalued, but we could not respond with anything.”

The recession led to a 5% cut in public spending and poverty reduction, which had been such a big success of the administration, stalled. Correa wanted to re-introduce the ‘Sucre’ but feared that to do so would “cause economic, social and political chaos”.

“We can’t do anything but maintain the dollarisation, being very aware of the restrictions: it’s like fighting in the ring of globalisation with a straitjacket,” Correa added. “It would be much easier to be able to devalue a little the currency in order to foment exports, limit imports and correct the external imbalance. Provinces at the borders have lost a lot of economic dynamism because we could not respond and address the imbalances in the external sector, like the drop in oil prices. We have had to constantly juggle.”

What Correa did not face was a financial crisis, which would have really tested dollarisation to its limits, but having introduced a strict domestic liquidity requirement on banks, a measure that brought billions back into Ecuador’s financial system, this was never likely. But with Scottish banking largely under external control, and the ‘Building a New Scotland’ paper proposing siphoning off financial regulation policy to the Scottish Central Bank (a de-democratisation that even the UK Government has not imposed), Correa’s strict regulation of the banking sector would not be repeated in Scotland.

Correa was replaced by his former vice-president Lenin Moreno in 2017, who moved the country to the right, and the possibility of ‘de-dollarisation’ disappeared for the time being. Under severe economic pressure, Ecuador signed a “structural adjustment” deal with the IMF in 2019. Now Ecuador is suffering under rising Federal Reserve interest rates, rapidly pushing up inflation in the Latin American nation even as unemployment rises, sparking mass protests in June.

Part 4: There is an alternative

The depressing picture I’ve painted in Part 1 and 2 about the likely trajectory of a sterlingised Scotland could easily be avoided. As many have previously argued (e.g. Craig Dalzell here), if the transition period to an independent Scotland, when the country would still be under the rubric of the Bank of England, was used to do all the work necessary to establish a Scottish currency on independence day (including foreign exchange reserves, which could be fully in place via debt and asset negotiations with rUK), the structural vulnerability described above would be largely neutralised.

There remains one final argument which requires attention: that every nation-state, currency-issuing or otherwise, is in a monetary straitjacket, and the recent collapse of ‘Trussonomics’ proves it. The speculative attack which led to Liz Truss’s downfall has resurrected austerity economics, now operating under the title of “sound money”, with the new occupants of both Number 10 and Number 11 Downing Street fully signed up advocates. Does this prove that there really is no alternative to rule by ‘the markets’?

The answer is a resounding ‘No’, and to understand why a tweet from Nick Macpherson, the UK’s most senior civil servant from 2005 to 2016 and now in the House of Lords, is very revealing. Macpherson gave the game away shortly after news of Kwasi Kwarteng’s sacking as Chancellor became official:

The Bank of England could have easily coped with a speculative attack on UK Government bonds by committing to buy as many gilts as required to force their price back down. Indeed, around the same time as the UK meltdown, the Bank of Japan did exactly that, and with complete success, and this is in a country with a public debt to GDP far higher than the UK’s (266%).

As Macpherson indicates, it was a deeply political move on Bailey’s part to set a 14 October deadline just two days before all BoE support (which began on 28 September) would be cut off, thereby threatening Truss with big financial trouble unless she began to unwind her ‘mini-budget’ completely. Indeed, the effect of Bank of England gilt purchases announced earlier in the week was to push down the cost of government borrowing.

“[The BoE] refused to extend its support beyond 14 October — even though its purchases of long-term government bonds were fully indemnified by the Treasury,” Narayana Kocherlakota writes in Bloomberg. “It’s hard to see how that decision aligned with the central bank’s financial-stability mandate, and easy to see how it contributed to the government’s demise.”

So, the lethal blow to Trussonomics was ultimately delivered not by the financial markets but by the BoE, which had good reason to be unhappy. Truss, who had spoken during the leadership campaign of reviewing the BoE’s mandate, was clearly working at cross-purposes with Bailey’s agenda of trying to get inflation down – he announced plans for Quantitative Tightening worth £80bn just a day before that ‘mini-budget’ which appeared designed to boost demand, especially among the richest. Plus, Kwarteng had made enemies at the Treasury by immediately sacking its veteran permanent secretary Sir Tom Scholar. This was the old guard of the British state roundly defeating a uniquely weak, ideologically contrarian government.

As economist Josh Ryan-Collins points out in an excellent piece in The Guardian, the demise of Trussonomics will be a “pyrrhic victory” for the left if it “leads to a re-embracing of the fiscal conservatism that has dominated British politics for most of the last quarter-century, together with an unquestioning faith that markets know best.”

He goes on to argue that this isn’t Britain’s “Greece moment” because “we are not facing a Greek-style sovereign-debt crisis. Indeed, a sovereign currency-issuing nation cannot default on its debt denominated in its own currency. Rather, it is facing an inflation-expectations crisis, in which investors lose confidence in the government’s ability to bring down prices. High inflation reduces the real value of government debt and will lead to higher interest rates that will push down their price. This is bad news for the investors who hold such debt, hence the sell-off of bonds.”

In place of fiscal conservatism, Ryan-Collins proposes the following:

- “Major public investment” to reduce inflationary pressures, such as through a national home retrofitting scheme

- Use tax policy to dampen inflation by targeting the excess cash of the rich, by “taxing unearned wealth, including from property, and environmentally damaging activity”.

- Co-ordinate fiscal and monetary policy so they are acting in sync, not at cross-purposes

- The de-financialisation of government debt so it is no longer used by financiers “as collateral to hedge their market positions”

Ryan-Collins is proposing this for a UK Labour Government, but it could also be an agenda for an independent Scottish Government, but only one that has a currency-issuing central bank.

Perhaps the most damning indictment of sterlingisation is that if Truss’s mini-budget fiasco had occurred while Scotland were independent, a sterlingised Scottish Government would have been unable to respond.

“In his recent speech to the SNP conference, Ian Blackford MP, the party’s Westminster leader, focused on the recent mini budget, arguing: ‘Your homes, your pensions, your incomes are not safe under Westminster control’,” Hardie writes. “Informal currency union would not protect Scots from the consequences of Kwasi Kwarteng’s impact on the gilt market, mortgages, pensions, or the currency.”

The Scottish independence movement – the vast majority of whom back a Scottish currency – should continue to loudly make that case and apply pressure on the Scottish Government until it sees sense. A Scottish currency is no guarantee that independence would see the country’s deeply embedded economic problems tackled. A monetarily sovereign independent government would still be perfectly capable of chronic mismanagement. But to have an independent country with a fighting chance of making even partial economic and social progress, monetary sovereignty is a pre-requisite. Another Scotland is still possible.

Images: Bank of England by George Rex via Wikimedia Commons CC BY-SA 2.0; Czech crown via Wikimedia Commons CC BY-SA International 4.0; Christian Lindner via Wikimedia Commons, CC BY-SA 3.0; Rafael Correa via Wikimedia Commons, CC BY-SA 2.0

.jpg){kind=link}

{kind=link}

.jpg){kind=link}

Further reading: Treasury orthodoxy: Fact or Fiction?, Nick Macpherson speech to Strand Group (KCL) in Edinburgh, November 1; Return to reality, Anton Muscatelli, sceptical.scot; Fantasy economics…, John McLaren, sceptical.scot and many more, including: First thoughts on the Scottish emergency budget review, Fraser nof Allander Institute

Ben Wray is co-author of ‘Scotland After Britain: The two souls of Scottish independence’, published by Verso (2022).

Leave a Reply