Let me congratulate you on becoming the first Finance Minister of a newly independent Scotland.

The Scottish Prime Minister has made an excellent choice! Given your new responsibilities, I hope you don’t mind me offering some words of advice. Ignore them as you see fit.

Your job is to ensure the economic stability of the newly independent Scotland. Deep reductions in living standards are not what the indyref voters expect. Looking out of the window, you notice that the world has not stopped. People largely continue as before, going to work, socialising and interacting with the outside world. Some people predicted an economic meltdown on the day after independence: this has evidently not happened.

While this is comforting, you must now engage with the task ahead. Your first priority is to maintain economic stability. You may think that this means not making dramatic policy changes immediately after independence, since it is important to maintain confidence. The last thing you want is for resources – labour and capital – to drain away to other jurisdictions. Nevertheless, as this letter lays out, you will have to confront new challenges, some of which may force policy changes.

The basics

So here is a picture of the economy that you inherited. The Scottish economy produced around £177 billion worth of goods and services in 2019, prior to the pandemic. Around £11 billion of this total came from oil and gas: a sector whose long-term future is in serious doubt both because of depleting reserves and climate change policy. So perhaps the £177 billion total flatters somewhat to deceive.

Per capita income was £32,400 including oil and gas and £30,800 if the offshore economy is ignored (Scottish Government, 2020). The Organisation for Economic Cooperation and Development (OECD) is the ‘rich countries’ club which monitors their performance across a range of economic and social indicators. Measured against these OECD countries, Scotland scores moderately well. As John McLaren puts it:

Although lying mid-table, Scotland can still be viewed as a relatively prosperous OECD nation. This ranking is likely to apply regardless of whether Scotland is part of the UK or independent (McLaren, 2019).

In terms of labour market participation, the UK is in the top quartile of OECD countries. In the first quarter of 2020, 75.6% of the UK’s working-age population was in employment. The latest data from the Office for National Statistics (ONS) shows that the Scottish rate is trailing the UK rate by around 2% (ONS, 2020). Nevertheless, Scotland’s employment rate would still be in the top third of OECD countries, leaving France (66%), Canada (64.7%), Spain (63.2%) and the USA (62.5%) trailing some distance behind. Scotland scores well in labour market participation.

Scotland also has a relatively low unemployment rate – the share of labour market participants currently looking for a job. Data from Eurostat for 2019 suggests that the unemployment rate in Scotland for those aged 16 to 74 ranked 25th lowest out of 89 ‘NUTS 1’ regions in the EU (Eurostat’s code for different sizes of regions, with NUTS 1 constituting ‘major socio-economic regions’). And on youth unemployment (16th) and long-term unemployment (24th), Scotland also scores well compared with other NUTS 1 regions (Eurostat 2019).

However, Scotland does not do well in the OECD income inequality ranking. Although it has a high employment rate, many workers are relatively poorly paid. In consequence, there is a larger spread between the incomes of the well paid and those of the poorly paid than in many other countries. The UK has the 9th highest income inequality rate among the 37 OECD countries. Inequality in Scotland is slightly less than the UK as a whole, largely because Scotland has fewer very ‘high earners’. Nevertheless, inequality is higher than in most OECD countries, giving the lie to that oft-repeated phrase of us all being ‘Jock Tamson’s Bairns’.

Because incomes are unequally distributed, so too are tax receipts. From Scotland’s total population of 4.5 million, around 2.7 million are in work. Of these, about 2.5 million pay income tax: the incomes of the missing 200,000 are less than the income tax personal allowance. Yet only 297,000 of Scotland’s taxpayers are higher rate taxpayers (with taxable income above £43,431 and less than £150,000) and a mere 14,000 are additional rate taxpayers (with taxable income above £150,000). Yet the additional rate group provide 16.6% of income tax revenue, while the higher rate group pays a further 39%. Scotland’s main source of tax revenue is dependent on a relatively small section of the population. Revenue from other major taxes like VAT and national insurance is much less concentrated, but you will have to bear in mind how changing tax rates and allowances may affect revenues, not necessarily in a good way.

Some would argue that focusing on incomes and GDP per head misses the point. Politicians should focus on maximising well-being rather than GDP. Indeed, as First Minister of the devolved Scottish Government, Nicola Sturgeon argued that Scotland should ‘redefine’ what it means to be a successful nation. Instead of aiming to maximise the output of goods and services, it should instead look to maximise ‘quality-of-life’ (BBC, 2020).

Those clever people at the OECD have amassed a cornucopia of data relating to quality-of-life across its component regions. Scotland scores well on ‘community’ (first in the UK, top 9% in OECD), ‘environment’ (fourth in the UK, top 22% in OECD), ‘access to services’ (third in the UK, top 10% in OECD) and ‘life satisfaction’ (first in the UK, top 37% in OECD). On the other hand, it scores badly on health (worst in the UK and in the bottom 37% in OECD) and safety (9th out of 12 in the UK and in the top 48% in OECD).

A mixture of good and bad

So, as the new Finance Minister of an independent Scotland, you would be taking control of an economy with a mixture of good and bad attributes across a range of indicators. This is true whether you adopt the conventional approach using indicators of output and the labour market, or if you focus instead on measures of well-being. Scotland’s performance has been by no means stellar, but neither is it seriously problematic.

The statistics on income and the labour market quoted previously were collected before the Covid-19 pandemic. You have now had a longer period to assess its negative effects on the Scottish economy. But as I write this letter, the path of economic recovery is unclear. We do not know whether the Scottish economy will grow more quickly during the remainder of this decade then it did between 2010 and 2020. It is also unclear how Scotland’s economic circumstances may affect the political economy of independence.

In taking the tiller after the independence bell has sounded, you will also be aware that the evidence suggests that people care more about losing something than they do about making an equivalent gain (Lineira et al, 2017; Tversky, 1991). So, unless voters value the realisation of independence more than they do the losses they experience if things go wrong, your political survival will partly depend on making sure things at least don’t get worse.

Having experienced drastic lifestyle change due to the pandemic, such as lockdown, remote working and home schooling, individuals may be willing to accept further substantial changes in their life with equanimity. On the other hand, the possibility of negative changes in circumstances may trigger the ‘loss’ response with the consequent draining away of support for your party and for independence.

The road ahead

What then faces you on the road ahead? Compared with being Finance Minister in the devolved Scottish Parliament, you have a much wider range of economic ‘levers’ at your disposal. However, finance ministers understand that there are limitations on their powers in a capitalist system 1 . This is because most of their powers relate to markets, and there are always two sides to a market.

When government intervention leads to increases in prices, buyers and sellers will tend to stand back. Thus, taxes which increase the price of labour will see employers looking for solutions that involve fewer workers, and workers looking for jobs where taxes are lower. Offering inward investors inducements to come to Scotland may not work if other countries are more generous with their inducements. The effects of these policies may only be at the margin, but the margin can matter a great deal if it makes the difference between people’s living standards improving or declining.

Another key difference from being the Finance Minister under devolution is that you previously relied on the UK government to maintain macroeconomic stability. Now you’re on your own. You must pay attention to balancing the national accounts – something you have not previously needed to think about.

Borrowing

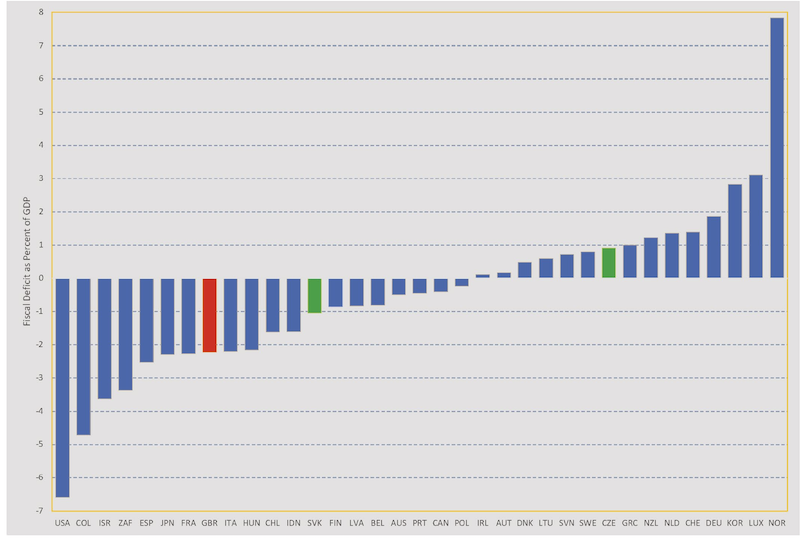

A key component of the national accounts is the fiscal balance – loosely the difference between government spending and taxes raised. Why? Because it is inexorably linked to the issue of state debt. And all of the evidence produced by the Scottish Government suggests that spending on public services exceeds the taxes raised in Scotland, by some distance (Scottish Government, 2019; see also the chapter by Roy and Eiser in this volume). If the new Scottish Government wants to maintain current spending levels, it could increase taxes. However, ramping up tax rates may not generate hoped-for increases in revenue for the reasons discussed above. The alternative is borrowing. How much will be needed is difficult to say: it will depend on the course of the economy post-Covid. The Institute for Fiscal Studies expects that the UK will borrow around £307 billion in 2020-21 (Emmerson et al, 2020). This is nearly 16% of GDP. The pre-pandemic forecast was 2%.

UK debt, turbocharged by the need to support the economy during the Covid pandemic, is likely to top 100% of GDP in 2020 (Emmerson et al, 2020). It was last at this level in 1950 in the aftermath of the Second World War and the establishment of the welfare state.

Yet although these are frightening numbers by recent standards, governments are finding it easy to borrow. Debt servicing costs – the interest that must be paid on borrowing – is low for most, but not all, countries. Debt service costs for the UK as a share of its tax revenues are at a 320-year low (IFS, 2020). Thus, although the pandemic has caused a huge spike in debt, the costs of servicing this debt are low. These costs may rise if interest rates rise, but at present this seems unlikely at least in the short- to medium-term.

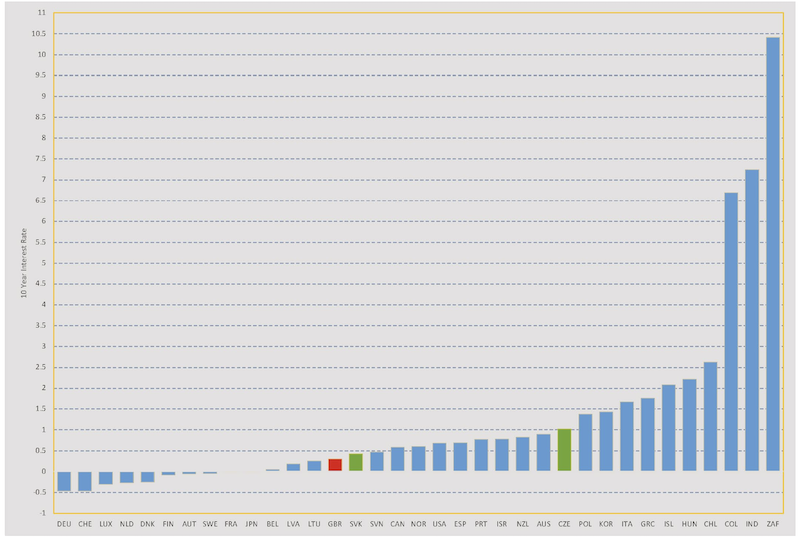

A useful guide to government borrowing costs is the interest rate on 10-year government bonds. Investors, many of them representing pension funds, assess countries’ ability to repay their debts at the interest rate they offer. They look at the tax regime in the country, its prospects for growth (and therefore increased tax revenue to repay its debts), how much debt it already has, how onerous are its debt servicing charges and how politically stable it is. Governments generally pay less for debt than companies, because sovereign governments have the power to tax their citizens.

If lenders are unwilling to buy bonds, governments selling the debt have to implicitly increase the interest rate that they offer. Figure 1 shows 10-year interest rates for OECD countries during the second quarter of 2020. Relatively few countries are now paying more than 2.5% for 10-year bonds. And some are charging lenders to deposit money in exchange for bonds, meaning negative interest rates.

Some countries such as Germany, Switzerland, Denmark, Finland and Austria are making money by borrowing – standing the usual rules of debt on their head. Lenders flock to these countries because of their reliability for repaying debt: a small reduction in the value of loans over 10 years offsets the risk of lending to less stable countries or to the private sector. It also implies an expectation that price inflation will be low in these countries, so that the value of their loans will not be further eroded by price increases.

The UK Government currently pays less than 0.5% on its 10-year bonds. This low rate explains why the cost of servicing the UK’s considerable debt is so low.

But the UK rate is higher than some European countries whose economic prospects are viewed more favourably. Interestingly, UK rates are very similar to those of the Slovak Republic, while the Czech Republic pays just under 1%. These latter two countries (highlighted in green in the figures) are of interest, because they separated from each other in 1993. You will be aware that, prior to Scotland’s separation from the rest of the UK, this is the most recent European case in which a state broke itself up.

OECD data on long-term interest rates for these countries starts in 2007. Since then, the Czech and Slovak rates have largely followed international trends. Neither country has had a sovereign debt crisis, where private investors are no longer willing to provide loans to government and a bailout is called in from an international organisation, usually the International Monetary Fund (IMF). Given that, unlike Scotland, neither country could be described as a fully-fledged market economy when they became independent, this is a substantial achievement.

The willingness of investors to lend depends on their assessment of risk. As Finance Minister, you will have to persuade the markets that lending to Scotland is relatively risk-free. One way to do this is to have robust and transparent policies and institutions to manage debt. This issue was discussed extensively by the Sustainable Growth Commission, which argued for rules and targets in relation to public borrowing (SGC, 2018). Of course, another form of reassurance is not to borrow very much relative to the tax revenues which you raise and use, partly to service these borrowings. One way to achieve this is to set long-term fiscal targets, an issue that the Sustainable Growth Commission also addressed.

Fiscal discipline

It might seem that discussion of fiscal discipline harks back to pre-Covid times. Covid has caused governments to borrow money on an unparalleled scale in peacetime. Some of the debt has been funded by printing money. This process is called quantitative easing (QE). It works when a country’s central bank buys government debt from financial institutions in exchange for cash, allowing these institutions to extend their lending to companies and individuals.

Although it has helped maintain economic activity, QE has also had less desirable consequences, including the rapid growth in house prices (Ryczkowski, 2019; Zhu et al, 2017) increasing inter-generational inequality by, for example, making home ownership more difficult for younger people.

Could an independent Scotland pursue QE as a means of maintaining demand during a pandemic? If it retained sterling, as was recommended by the Sustainable Growth Commission at least in the short run, it would not have any say over monetary policy, including QE. It would be exposed to the implications of Bank of England QE decisions. So if downturns in the Scottish economy occurred at the same time as those in the rest of the UK (as is likely given their close trade ties), then monetary policy decisions taken by the Bank of England would likely align with those that a Scottish central bank would have taken (if they shared a monetary framework). Under these circumstances, Finance Minister, QE would not be an option open to you. Even if Scotland had its own central bank, markets would expect its tactical decisions over monetary policy to be independent of your influence.

A central bank would be necessary if Scotland created its own currency.

Finance ministers in countries with their own currencies understand that borrowing from foreign investors has different implications from domestic borrowing. Issuing debt in a foreign currency (say the pound), would make it easier for the Scottish Government to borrow and at lower rates. Such demand might stem from foreign banks and pension funds wishing to spread their risks across different countries. However, the Scottish Government cannot tax foreign investors in the same way that it can tax domestic investors if its debt servicing costs are heavy.

In addition, if the Scottish currency depreciates relative to other currencies, the real costs of debt repayment to foreigners increases. And if foreign lenders sell Scottish Government bonds back to Scotland because, say, they have lost faith in the Scottish Government, there will be a decline in Scotland’s foreign exchange reserves. This process will also happen as bonds mature. Having sufficient foreign exchange reserves to cover short-term debt repayments is one of the criteria that Roubini and Manasse (2009) highlight as a characteristic of countries which avoid sovereign debt crises. I hope you have a plan to deal with this issue.

A further difficulty for you will arise if the Scottish Government decides that its longterm ambition is to join the EU. There will then need to be a plan for joining the Euro. This is not necessarily a quick process. Joining the EU will only occur after the entry conditions have been satisfied. After joining the EU, the process for joining the Euro could take a long time. Only seven of the 13 Member States who joined the EU since 2004 have joined the euro area. The most recent was Lithuania in 2015.

The current conditions for joining involve (1) price stability, (2) the public finances, (3) convergence and (4) exchange rate stability. Whether the EU will change these over the next few years is anybody’s guess, but it would be best to assume that they won’t. In which case, you should set out a long-term strategy whereby you would meet the conditions. It won’t be easy to meet the public finances criteria – not being under the ‘excessive deficit’ procedure, especially if your government decides it does not want to make sustainable economic growth its primary objective. Compared with substantive hikes in tax rates across the board (you couldn’t just rely on squeezing more tax from the relatively affluent), economic growth is a more painless way of increasing tax revenues. At least you will have time to figure all of this out. But it is important to lay out your plans early on. Politicians and the media are easily distracted by the issue of the day.

Conclusion

These issues may seem complex to you as a fledgling Finance Minister, but many small countries handle them on a day-to-day basis. Certainly, dealing with debt markets and foreign exchange transactions would mark a huge increase in the range of issues that you would have to deal with compared with the Finance Minister role under devolution.

One policy consideration which you might want to explore would be to encourage higher levels of domestic saving to reduce dependence on foreign sources of loan funds. It is interesting that the increase in UK domestic debt has been mirrored by an almost identical increase in household saving during the pandemic as households were effectively forced to save (Young et al, 2020). This means that the pandemic has not increased the level of UK indebtedness to foreign actors. This balance is something that you will have to watch carefully since it may colour the attitude of lenders, should you need to borrow.

But again, there would be trade-offs. For instance, increased saving might depress demand in the economy, leading to lower levels of activity. And of course these considerations would come in addition to your duties to ensure that the economy remains on a stable footing and that the labour market functions well in matching workers with jobs and creating new opportunities for employment.

And even though, with Scotland as an independent country, your policy options would be much greater, you have to be constantly aware of the trade-offs involved and the limitations on your power to influence the choices made by workers and by companies. You can at least take comfort from the fact that less prosperous nations with less well-developed institutions than Scotland manage these issues without the roof falling in.

• This forms Chapter 5 of the new e-book Scotland’s New Choice: Independence after Brexit published by the Centre on Constitutional Change and edited by Eve Hepburn, Michael Keating and Nicola McEwen

See also: Long-term economic benefits of independence, LSE Blog (removed “temporarily” after Treasury objections’)

Leave a Reply