It seems common to assume that we’re faced with a straight choice on tuition fees, where the state either funds the whole of everyone’s tuition costs, or all students have to take out a loan for £9,250 a year.

It’s a perspective stuck in a binary choice between whatever-we-do-now-in-Scotland and whatever-they-do-now-in-England. Other options are of course available:

A starting point

The simplest alternatives for fees are:

- setting the fee level at some number more than zero, but less than £9,250;

- means-testing fees; or

- some combination of these two.

There’s a fairly common argument that any move away from free tuition inevitably means Scotland would end up where England is: the slippery slope perspective. That puzzles me, because we would only end up there if that was what the politicians we elected chose. It seems to assume we can trust them to keep it free, but not to maintain any alternative position. On this thinking, tuition fees are an addictive drug, from which governments must be kept away at all costs. I’ll come back to that at the end.

If you reject this straitjacket, and believe that the Scottish political system is capable of managing other things, what might the alternatives be, and what would they mean for students?

Note: I’m not advocating a specific model here, but demonstrating one different way things could work, as a starting point for a less constrained debate. There are more radical ideas out there (here’s one), involving more fundamental change. All I want to show is the space for alternative outcomes, just within the current broad general approach.

Living cost support matters

There’s no point designing a student funding system which only looks at one part of the story.

If you are only interested in thinking about fees in isolation, and don’t care much about living cost support, especially for low-income students, then look away now. You and I are never going to have a mutually rewarding conversation about this.

A lot of people in Scotland at this point suggest that living costs are a secondary (or even non-) issue, because students can always live with their parents and/or work their way through. I disagree for the reasons set out in Footnote 1.

The modelling below assumes decisions on living costs are as important as fees, should be interlinked, and looks at combined effects.

Fees: upfront or deferred?

Even the most vigorously ideological advocates of tuition fees recognise that students tend not to have money at the moment. It is very rare to find anyone, not even Milton Friedman, advocating unassisted upfront charges (Footnote 2 describes the UK government’s short experiment with this).

Thus, in no part of the UK do first-time students now have to find the cost of their fees from their or their families’ existing resources. With a few exceptions in Scotland and elsewhere, higher education is free at the point of entry for all first-time undergraduate students in the UK, because at a minimum they can take out a government-subsidised student loan to defer the full cost of their fees until they are earning above a certain level.

It’s hard to over-stress this point for readers in Scotland, where it still seems to be widely believed that students in England have had no choice but to find £9,000 a year from their families. Had that been the case, the system there would simply have collapsed. It is precisely because fee costs are deferred that debt is so high in England.

So the model assumes that any fee is matched £ for £ by a government subsidised loan and that, as in other UK systems, the fee loan (a) would be repayable contingent on earnings, in the same way as maintenance borrowing is now, and (b) is added to any maintenance loan to form a single debt, so that no-one is paying off two loans in parallel.

Debt aversion

Regardless of any evidence from England (Footnote 3), it is possible that debt aversion should be a major concern for Scottish policy makers. In that case, however, we should already be worrying.

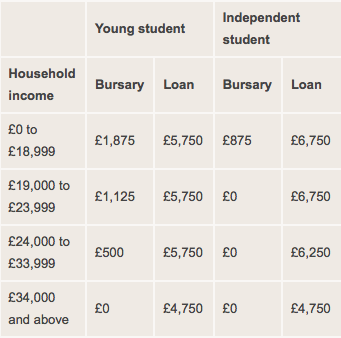

Living cost support for low-income Scottish students is now provided largely through loans, because grants are relatively low. Here’s the figures for support from the Student Awards Agency Scotland (SAAS) for 2016-17.

The model below illustrates how in a system which includes some fee-paying, low-income students can still have less debt than in one with free tuition, while protecting the value of their total living cost support.

The scale of student debt in Scotland and its distribution

Around £500 million is now borrowed each year by Scottish students. At the moment, annual borrowing is skewed towards those from lower-income households, for two reasons:

- they borrow more on average, and

- they are more likely to make use of student loans.

As a result, over half of all student loan is taken out each year by students declaring a household income below £34,000, although fewer than half of students fall into that group.

The current statistics don’t allow us to differentiate amongst those with incomes over £34,000. But looking at earlier data, there’s a good chance that there’s a similar skewing of debt within the higher income group, towards middle-income households and away from the highest income ones.

The model removes the current built-in assumption that the highest debts should be taken on by those from the lowest incomes, again while protecting current total spending.

What could be different?

Put simply, we could move the debt around, so that more of this £500 million is taken out by students from higher-income backgrounds, and less by those from lower-income ones.

That means finding more to spend on grant, by spending less on fee subsidies, and expecting those at higher incomes to borrow some of their fee cost.

Mechanisms

There are in essence three ways to get this effect.

- Means-test the fee.

- Apply the fee to everyone, but then have a separate means-tested fee grant which immediately wipes it out for lower-income students.

- Apply the fee to everyone, but then build a means-tested off-setting amount into the living cost grant, before making any other increases.

Different mechanisms would have different implications for practical administration, public understanding/presentation, student behaviour and the detail of public finances. But they would all provide an identical boost to the amount of grant provided at lower incomes for the same level of fee.

One basic model

The model below asks students from the highest income households to borrow one half of the average cost of a university place in Scotland. So students from these households would be offered a government-subsidised fee loan to cover a fee of £3,500 a year. The cash released from tuition fee subsidies would be put back into grants.

How much would a £3,500 fee raise?

SAAS currently supports around 140,000 students, of whom around 15,000 are from the EU. I’ll concentrate for now on moving the public subsidy around between the 125,000 Scottish students. A separate section below considers EU students.

If Scottish students from the highest quarter of student-providing households by income were liable for the fee, it would notionally release around £110m a year from tuition fee subsidies (125,000 x 25% x £3,500).

I can’t say what the income cut-off would be, because the Scottish data on students is now too aggregate to show that. Looking at figures for years before 2013, when more detail was provided, I’d guess it would be somewhere between £50,000 and £60,000 of household income (around the highest 15-20% of all households in Scotland by income, after equivalising for a family of 2 adults and 2 children).

How could the money saved on fee subsidies at high incomes be used to bring down debt at lower incomes?

I’ll spend the money on substantially increasing means-tested maintenance grants, on which we now spend only £55m a year.

It would cost ca £30m to switch £1,000 of living cost support from loan to grant for those on the Young Student Bursary.

I’ll spend a further ca £40m on giving independent students (for example, those over 25, or who are parents, or married/in a partnership) the same bursary as young ones, and bringing down their debt, because these students in Scotland are on a much less generous grant and a higher loan, and there’s really no good way to justify that.

I’ll also spend ca £15m on a new £1,000 grant for students from households between £34,000 and £45,000, because these families, who are not awash with cash, are expected to find much more out of pocket help for their children in Scotland than is the case in the rest of the UK and that’s a concern: more here.

The net annual effect on individual students at different incomes would be:

- Young students with incomes below £34,000 would gain £1000 in grant and lose £1000 in debt, with no change in the total value of their living cost support.

- Those with incomes between £34,000 and £45,000 would gain £1,000 in grant and therefore £1,000 in total living cost support, with no change in debt.

- Nothing would change for those between £45,000 and the fee liability point.

- Those liable for fees would have £3,500 more debt a year and no change to living cost support.

- For mature students it’s a similar picture, except that they would gain more grant and lose more debt.

Using this approach, all students are now offered the same living cost loan (£4,750), with cash grant used to do any additional income-based targeting

I’ve spent approaching £90m. I assume that, due to things I’ve failed to take into account, income wouldn’t be as high and expenditure would be higher, so my spending plans may still be a bit ambitious on this level of fee. But they will be in the right general area. If students from the wealthiest quarter of households were expected to borrow £3,500 a year of their tuition cost, it seems likely that we could nearly treble our spending on maintenance grants.

The effect on the new fee payers

Total debt for those at high incomes would come to a maximum of £8,250 a year. Two points about that. First, in practice many of these students would only have a £3,500 annual debt because living cost debt take-up is lower in this group, presumably because many have all their living costs met by their parents.

But the second is the more important. Low income mature students are already expected to incur £6,750 in living cost debt – and most do. If you have managed in recent years not to be outraged at the reality of a £6,750 annual debt for most mature students with no income, you are not in strong position to be outraged now at a theoretical maximum debt of £8,250 a year for students from high income families which many won’t actually incur.

Is this a good model?

This would be a pretty clunky way to do things. The Scottish system already incorporates large step changes in entitlement, and it’s not an ideal approach. However, because the data comes packaged that way, it’s hard to model anything without copying that.

The point of this model is not to advocate it in this precise form, but to bring out what scale of change would be possible for a particular form of fee liability.

A more radical, and carefully argued and well-evidenced, rearrangement of fee and grant subsidies has been proposed for Wales by the Diamond Committee. The Welsh Government has accepted the recommendations and recently finished consulting on the detail of implementing it. The change has cross-party support, and support from NUS Wales and Universities Wales. Anyone interested in this debate should read that report (here), as a further example of the range of possibilities.

What about other objections to fees?

If your objection to fees is that higher education is a public good and therefore students shouldn’t have to contribute on principle, I have bad news. Scotland crossed that ideological bridge a long time ago and is now £500m a year into that territory, because all student loan debt is a form of student contribution, whether it’s for living costs or fees. Moreover, there is no realistic chance that the Scottish Government is going to reduce its reliance on student loans to underwrite the higher education system. £500m is roughly the annual cost of the whole FE system, or 1p on the basic rate of income tax.

A separate objection to fees is that they create a ‘weakest to the wall’ market in higher education. That’s not a necessary effect in the model above, in which the SFC continues to decide where the funded places are, and fully funds the fees of three-quarters of Scottish undergraduate students and half the cost of the rest. It is entirely possible to seek a fee contribution from some students (or even all) in a system as planned as the current one, without moving to a quasi-voucher market.

Another objection is that fees change the nature of higher education, converting what should be a purely educational relationship into a purchase, and positioning students as consumers (some people are for this, but many are not). Around half of students in Scottish universities already pay fees, including many on full-time undergraduate courses (overseas students, rUK students). Many others are already taking out large loans to pay for their living costs. Would asking some, or even all, Scottish undergraduate students to borrow to cover some of the cost of tuition create a dramatic cultural shift from where we already are? That’s debatable at best, I think.

But even if you believe that all the things above would be unavoidable and undesirable, is the price now being paid to avoid them defensible? In order to shelter everyone from any fee at all, we have designed a system which means student debt has to be shouldered disproportionately by those from lower incomes, while people from the most well-off backgrounds are routinely leaving university debt free. It’s the least well-off students bearing most of the cost of these principles.

Investing in grants vs other things

One of the arguments often made for fees is that access to HE remains socially skewed and it would be better, and fairer, to subsidise HE students less and spend more on levels of education which everyone uses. The model above doesn’t address that, because it doesn’t release any cash, it just moves it around between existing students.

The model also therefore doesn’t deal with the relative under-supply of places in Scotland compared to other parts of the UK. A thousand extra places fully funded for fees and grant would cost around £10m. Nor does the model offer universities any additional funding per student: increasing university spending has often (though not always) been behind fee rises.

To deal with these issues as well in any serious way would mean a higher fee, and/or one which was less heavily means-tested, and/or ceasing to provide EU students with free tuition (recalling that none of the sums above included them).

SAAS funds just under 15,000 EU students. The total current spending on them is around £100m a year (15,000 x £7,000: they cannot claim maintenance grant). We don’t know yet what the Scottish Government will decide to do about this group.

In 2010-11, the SG was actively seeking ways to charge these students at least something (here). My assumption is that, once EU law ceases to apply and once the current commitment to the 2017 and 2018 entry cohorts has been met, the SG will return to the issue of how it can reduce its spending on this group in some way, so that some or all of the cash is available for other things. At a time other things are under pressure, the sum at stake simply looks too large at first sight to be affordable as a voluntary symbolic gesture.

Where next?

One of the great campaigning coups of the past 20 years has been the success with which so many people have been persuaded that free tuition is essential to widening access and that defending it must be given absolute priority over improving (or even just protecting) levels of student grant. Thus grants in Scotland were cut by a third in 2013 with the support of NUS Scotland, and no outcry beyond the parliamentary opposition parties. Grants are important too, it is sometimes conceded, but not so important we should give an inch on free tuition to spend more on them. According to this view, the only proper way to increase grants is by finding the cash from some other budget, or more tax, and until that happens it is better to put up with what we have than to raid the fee budget.

I don’t expect any real shift in policy here or even in what people are prepared to debate. The SNP, the Scottish Greens, Scottish Labour and the Liberal Democrats all supported free tuition in the 2016 Holyrood elections (though at least the Conservatives, Labour and Liberal Democrats also mentioned increasing means-tested grants, and the SNP said it would “work to improve” them). The Conservative offering on fees was much more cautious than the model above, limited to something like the old graduate endowment, and would have raised a relatively small amount, and not for several years.

The appearance of any proposal like the one discussed here tends to trigger Spanish Inquisition-like questioning of Scottish opposition politicians about whether they will rule out tuition fees (grants don’t get a look in), with a moment’s hesitancy being taken as political death. This – for the avoidance of doubt – is an absolutely brilliant state of affairs for people whose parents can fund them through university but much worse news for people whose parents can’t.

This positioning of tuition fees as a box which must never be opened even a crack benefits one section of society. It’s the one I know best, and it has always been good at identifying high-minded arguments in defence of its own interests. But rarely so successful as in this case at persuading other people that they must leave their barricade neglected, and come and defend this one instead. It’s been a rather one-sided vision of solidarity so far.

But here we are. The maths of a more even sharing of debt among students in Scotland is really pretty easy. The politics look as impossible as ever.

Footnote 1: Living costs don’t matter as much as fees because …

Students can live at home: (a) no, they can’t all do that, (b) even for those who can, it will not always be a particularly good idea and (c) even when it’s a good option, those students still need to be fed, to travel (especially, often, travel) and to have clothes, books and so on, and it’s not reasonable to expect families on low incomes to absorb these costs unaided.

Also, that students can work is not a killer argument against the equal importance of living cost support. There’s a growing literature on the impact of working, especially in term-time. It’s not all discouraging: some types of working, at some level, for some people, appear to be fine. But the overwhelming message is that those students who don’t take on paid employment, especially in term, will tend to get more out of higher education, academically and in other ways.

But there’s a more fundamental problem with saying that fee loans are a problem, but maintenance loans aren’t, because people can work. It confuses the income and expenditure sides of the equation. Logically, you might as well say fee loans wouldn’t be an issue, given a high enough level of grant, because people could work to pay their fees. Unless you accept the second of these arguments, you can’t use the first.

Footnote 2: Actual upfront fees – the 1998 reforms

In 1998, the UK government introduced an upfront yearly fee of £1,000. It was means-tested (this is generally forgotten), so that – roughly – the top third by income paid the whole amount, the middle third some of it, and the lowest third by income, nothing. The dedicated fee loan had not yet been invented (though living cost loans were boosted with the idea people might choose to use some of the extra amount borrowed to cover the cost). The change was very unpopular with those who had to pay, and the way it was discussed obscured that many paid nothing or only part. It was also accompanied by the abolition of grants, but that attracted much less fuss, as did their reintroduction in 2004.

The 1999 Scottish elections were dominated by 1998 fee regime and the sense that fees must be an immediate cost to families persists in Scotland still. However, when fees ceased to be means-tested in 2006, the UK government also enabled them to be deferred using a government subsidised loan. In passing, this means that nowhere in the UK since 1962 have first-time full-time low-income students been expected to find the cost of an upfront fee with no form of government help. But you could be forgiven for not knowing that, from the political rhetoric.

Footnote 3: Debt effects in England

Researchers looking at the statistics, and interviewing students, have discovered a high degree of willingness (not necesssarily enthusiasm, just willingness) to borrow among young students of all backgrounds in England. Participation rates there, including for those from disadvantaged backgrounds, have increased at least as quickly as in Scotland. This is not the same as saying no-one, anywhere has ever been deterred, and there’s more evidence that older, especially part-time, students are more debt averse. But the last 20 years of data from England (and comparisons with Scotland) on participation levels and access have generally not been as helpful to advocates of free tuition as they might have hoped.

First published on the author’s own site

Photo of Education Secretary John Swinney at Heriot Watt courtesy of Scottish Government via Flickr CC BY-NC 2.0

Leave a Reply