Brexit has changed many of the calculations around the implications of Scottish independence in the European Union compared to 2014, not least the question of borders.

That the Scottish Government has been loath to analyse the border question is not surprising – it’s a very tricky one. But now the UK has left the EU – and in just over four months will leave the EU’s single market and customs union, with or without a deal, it should not be left to one side any longer.

Some have argued that independence is just the mirror image of Brexit – leaving a union is damaging in either case. But the two unions are not the same – and there are both differences and similarities (as I’ve argued elsewhere). On borders, however, the two do look, unsurprisingly, similar. New barriers to trade between an independent Scotland in the EU and the rest of the UK (rUK) would hit trade with knock-on implications for growth unless there were offsetting advantages (leaving aside, for purposes of this piece, the other wider macro-economic and welfare state impacts of, and debates on, independence).

Impact of the EU border

A whole range of studies have estimated the hit to the UK from Brexit – including a recent Scottish Government one suggesting the sort of free trade deal the UK government seeks with the EU could knock over 6% off Scotland’s GDP over ten years (compared to staying in the EU). A study by the Fraser of Allander Institute (FAI) in 2016 suggested under a WTO, ‘no deal’ Brexit, Scotland’s GDP could be hit by 5% over a decade – more if productivity impacts are taken into account.

One difference to Brexit in looking at the border question for an independent Scotland is that, unlike the UK, which has left the EU without joining anything else, Scotland would leave the UK and aim to re-join the EU (which I’ve argued elsewhere could conceivably happen within 4 to 5 years). So, barriers to trade would go up between an independent Scotland in the EU and rUK – but they would decline between Scotland and the EU once it was a full member state and back in the EU’s single market. But Scotland exports three times more to rUK than to the EU so an absence of trade barriers with the EU will not fully compensate for those going up with rUK.

The most recent export statistics for Scotland are for 2018 (with all the provisos about the quality of the survey data it rests on). They show that 60% of Scotland’s trade is with rUK, 19% with EU and 21% non-EU markets. So, in essence 60% of Scotland’s export trade could be hit by tariff and non-tariff barriers (both customs and regulatory) while the 19% with the EU would benefit from barriers to UK-EU trade (starting in 2021) being removed.

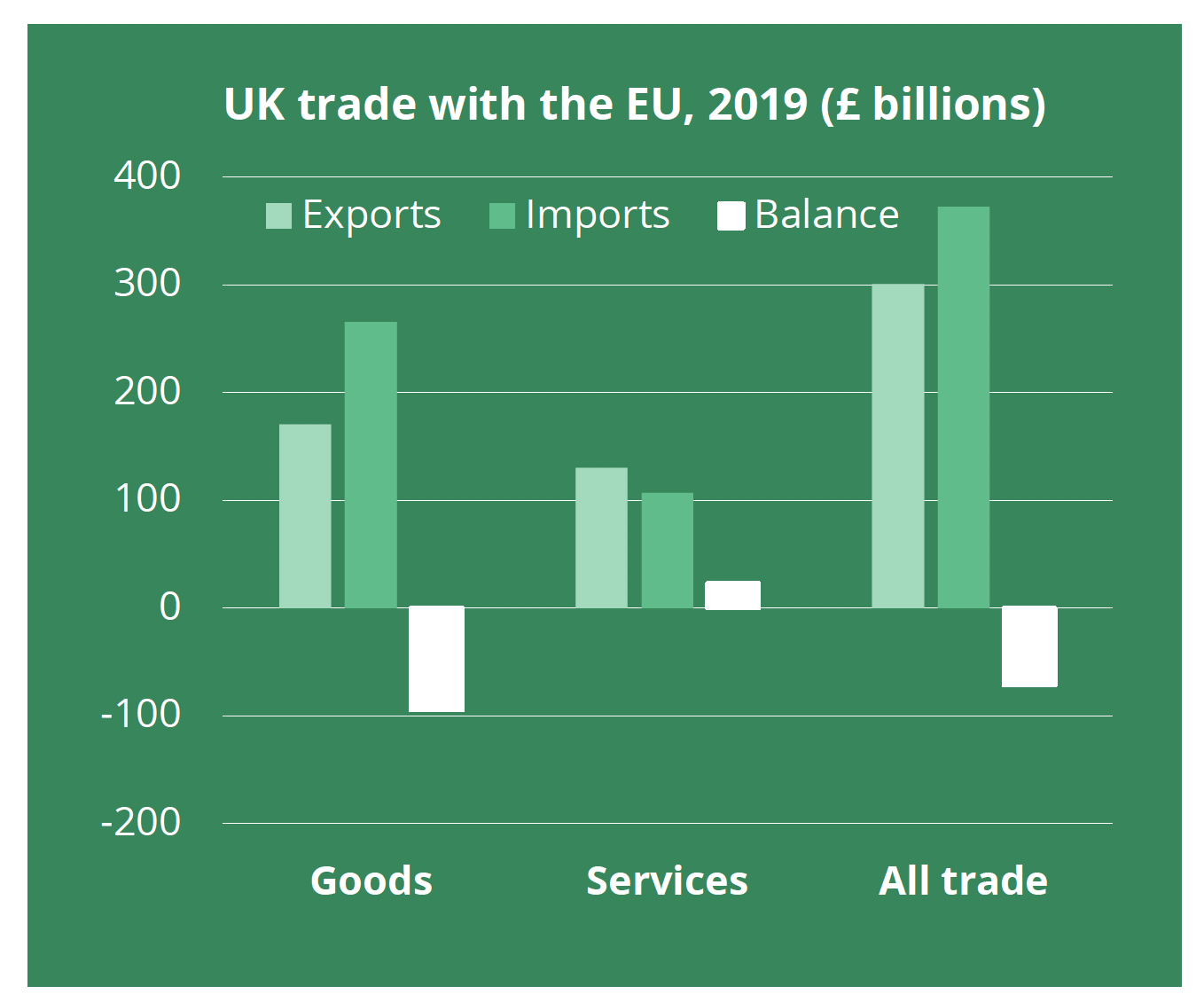

The UK’s exports to the EU in 2018 were just over 45% of its total exports. So, the share of exports hit by trade barriers would be quite similar for Scotland with independence as it is for the UK with Brexit – with a net amount of 41% of exports negatively affected. Of course, the two are not identical – impact will depend on the structure of trade and that of each economy and on other dynamic factors including migration and foreign direct investment (FDI) – and longer run trends over time. But it is hard to look at the scale of the challenge and not anticipate some negative growth effects in the shorter term.

And if there is a basic free trade agreement between the UK and EU this autumn (or even if trade goes ahead on a ‘no deal’ WTO basis) then the two cases are symmetric in the trade barriers they will face. The harder border that the UK will face with the EU, with costly regulatory and customs checks, is the same border i.e. the EU external border, that it will face vis-a-vis an independent Scotland in the EU.

Of course, this picture is complicated by the special position of Northern Ireland which remains effectively in the EU’s single market for goods. But Northern Ireland is just a small part of Scotland’s-rUK trade – and poses a cautionary tale on the bureaucracy and costs involved in having even a partial EU border with Britain.

Scotland’s export profile

Delve into the statistics a little further and there are some broad similarities in Scotland’s export trade with the EU, compared to UK-EU trade, and some notable differences in Scotland-rUK exports.

Almost 48% of Scotland’s international exports went to the EU in 2018, while 45% of UK exports went to the EU. Add in Norway and Switzerland, and half of Scotland’s exports went to countries in the EU single market – with single market countries accounting for eight out of Scotland’s top ten export destinations (the largest single country being the US – and Brazil coming in at number ten).

The UK and Scotland also have a similar list of largest export markets. The UK’s top five markets in 2019 were: the US, Germany, France, Netherlands, Ireland. Scotland’s top five in 2018 were: the US, France, the Netherlands, Germany and Belgium. Services accounted for about 38% of the UK’s international exports in 2019 and 36% of Scotland’s international exports in 2018. So, there are some notable similarities here – and both the UK and Scotland’s largest export market by far is the EU.

One question that has come up in the independence debate is how fast, and in what way, the structure of Scottish trade would change after independence – including a likely restructuring of trade dependence away from the UK (as happened over decades in the case of Ireland). This depends too on broader macro-economic and industrial strategy questions, choices and challenges for an independent Scotland. But, again, this needs analysing and spelling out what the potential scenarios are.

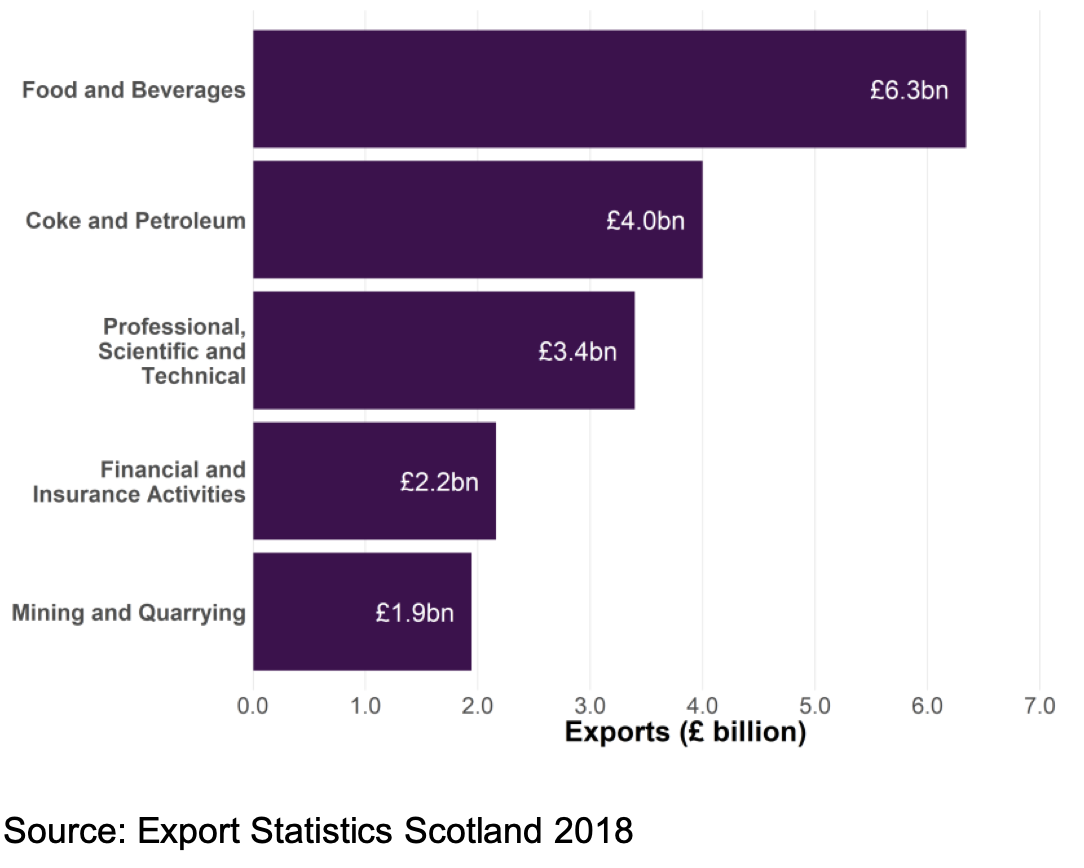

It is worth observing in that context that Scotland’s international exports are dominated by large companies: they account for 58% of all international exports, with medium-sized firms providing 25% and small firms (under 50 employees) accounting for only 18%). Any green economic development strategy will need to take the dominance of large firms in exports into account too.

Services trade with rUK as a challenge

Unlike Scotland’s international exports, as the FAI pointed out in a blog in February, Scotland’s trade with rUK is much more focused on services – with 58% of Scotland’s exports to rUK accounted for by these, 11% by utilities and 22% by manufacturing. FAI argues that Scotland “has increasingly become ever more of a satellite regional economy of the UK”. Whether and how, and over what time period, independence would change this (and with what costs and benefits) is, of course, the fundamental question.

In terms of the impact of borders, if Scotland is independent in the EU, this services dominance in Scottish-rUK trade may cut both ways. In general, trade deals focus much more on liberalising trade in goods than services. So, the dominance of services trade between Scotland and rUK looks worrying (if EU-UK trade barriers are higher in services than in goods (see an in-depth 2018 paper by Sam Lowe on Brexit’s likely impacts on different service sectors for the scale of potential impacts – they are not small). Any basic UK-EU trade deal that may be agreed this autumn is likely to reflect this general focus of international trade deals i.e. provide more access for goods than services – even if the EU grants so-called equivalence for (some/most of) UK financial services. Equally, as David Bell has argued, there may be service sectors where the EU single market is not complete and where it could be feasible for Scotland to do separate sector-by-sector deals with rUK – but the extent of this is likely to be limited.

Scotland would also benefit, in supplying services, if it stays in the UK-Ireland common travel area – since that effectively allows free movement within the UK and Republic of Ireland (helpful for the supply of services). At the same time, it would benefit from becoming part, once again, of free movement of people within the EU – fundamental for Scotland’s future demographic growth as the Scottish government argued in its paper on migration at the start of 2020. Benefitting both from EU free movement and from being in the common travel area looks like a clear win-win for an independent Scotland.

Foreign Direct Investment

There are other likely impacts of Scotland rejoining the EU, not least in FDI. There have been various studies looking at the likely negative impacts for the UK, given Brexit, on inward FDI into the UK, given it will no longer offer barrier-free access to the EU’s single market nor allow frictionless just-in-time supply chains.

One LSE study in 2016 estimated that EU membership increased FDI by 28% on average. And the Financial Times calculated in 2019 that, in the three years since the Brexit vote, greenfield investment had dropped by 19%.

An independent Scotland in the EU might then be expected to benefit from higher FDI and potential positive impacts on productivity. But, in considering the impact of FDI on costs of borders versus benefits of EU membership, the likely size of that higher FDI would need to be estimated compared to any potential reduction in rUK investment into Scotland (if trade barriers did reduce it whereas access to the EU’s single market via investment in Scotland should increase it).

Borders cannot Be Wished Away

Looking back, despite the 2014 debate about how easily or not an independent Scotland could re-join or even stay in the EU, the arguments were much more straightforward then. Both economically and politically, a scenario where both Scotland and rUK were EU member states would have been much more straightforward than the likely scenario now (unless the UK re-joins the EU) of an EU external border running between Scotland and rUK.

How this border will be handled and its potential economic impacts need some serious analysis from the Scottish Government, not least as the future UK-EU trade relationship becomes clearer this autumn. Overall, the fact that Scotland’s trade with rUK is three times that with the EU means it looks like the short- term economic impact of a harder border would be negative.

But some of those negative impacts might be at least partially offset by benefits from migration and free movement of people, and by FDI. Beyond that, there are longer term questions to be answered as to the likely future trajectory of the Scottish, EU and rUK economies – both in terms of growth, and in structural changes in moving to net-zero as fast as possible, as well as in terms of wider industrial strategy and quality of life goals (the “well-being economy.”)

The potential shorter and longer-term economic transition and structural change Scotland faces as an independent state within the EU, while rUK is outside post-Brexit, needs careful economic analysis and an understanding of likely costs and benefits. What it does not need is a studied looking away from the challenging economics of a Scotland-rUK border.

Image by Taras Young, via Wikimedia Commons, CC BY-SA 4.0

{kind=link}

Figures from House of Commons Library and Scottish Government

Leave a Reply to Jo beth Cancel reply