Both £33,000 and £26,000 have been quoted as the threshold below which Scottish taxpayers will pay less tax as a result of the December 14 tax policy announcements. But which figure is correct?

Undoubtedly on the tax side the big announcements related to changes to income tax in Scotland.

Derek MacKay announced that his draft budget proposed:

- Introducing a new ‘starter’ rate of income tax of 19% on incomes between the Personal Allowance (£11,850 in 18/19) and £13,850

- The Basic Rate will be maintained at 20% on incomes between £13,850 and £24,000

- A new Intermediate Rate of 21% will be introduced on incomes from £24,000 to £44,273

- The Higher Rate threshold will be increased to 41%, whilst the Additional Rate will be increased from 45 to 46%.

The Scottish Fiscal Commission estimates that these tax decisions will raise around £164 million of additional revenues for the Scottish budget in 2018/19.

But who will pay more and who will pay less as a result of these tax decisions?

The importance of baselines

In its Budget, the Scottish Government says: “When combined with the increase in the Personal Allowance next year, these proposals mean that nobody earning less than £33,000 will pay more income tax in 2018-19 than they do this year.”

The Scottish Fiscal Commission in its Fiscal Forecast report states: “All taxpayers with gross incomes below £26,000, in 2018-19, will see their tax liabilities reduce by a maximum of £20.”

The key difference is the policy baseline that today’s announcements are compared to.

Under the Scottish Government’s proposed income tax policy, everyone earning under £33k will pay less tax in 2018/19 than they did this year (2017/18).

BUT part of this is due to the increase in Personal Allowance, which would have happened anyway, i.e. irrespective of any announcement made by Mr Mackay today. The increase in the Personal Allowance from £11,500 to £11,850 saves a typical taxpayer (i.e. all taxpayers earning less than £100,000) £70 per year.

Taking the personal allowance rise into account, it is more accurate to say that the policies announced by the Government on 14 December mean that everyone earning less than £26k will pay less tax in 2018/19 than they would have done without today’s tax announcements.

Given that the correct baseline to compare to is the counterfactual estimate of what Scottish taxpayers would have paid in 2018/19 in the absence of the Scottish Government’s announcement today, what does today’s announcement mean for taxpayers with different incomes? This is summarised in the table below.

Impact of today’s income tax policy announcements

| Income | Amount better/ worse off (£) | Change in after tax income (%) |

| £15,000 | £20 | 0.13% |

| £20,000 | £20 | 0.10% |

| £25,000 | £10 | 0.04% |

| £30,000 | -£40 | -0.13% |

| £40,000 | -£140 | -0.35% |

| £50,000 | -£240 | -0.48% |

| £75,000 | -£490 | -0.65% |

| £100,000 | -£740 | -0.74% |

| £150,000 | -£1,359 | -0.91% |

| £200,000 | -£1,859 | -0.93% |

Going forward

Today was the opportunity for the Scottish Government to unveil their proposals for how the new tax powers of the Scottish Parliament should be used.

But, as with any minority government, the Scottish Government now require to get the consent of at least one other party in order to be able to pass their budget early next year.

This means that there is scope for the proposals announced today to change between now and the budget bill being passed in February.

First published by Fraser of Allander Institute

Readers should also look at the FAI analysis of the Scottish Fiscal Commission 5-year forecasts

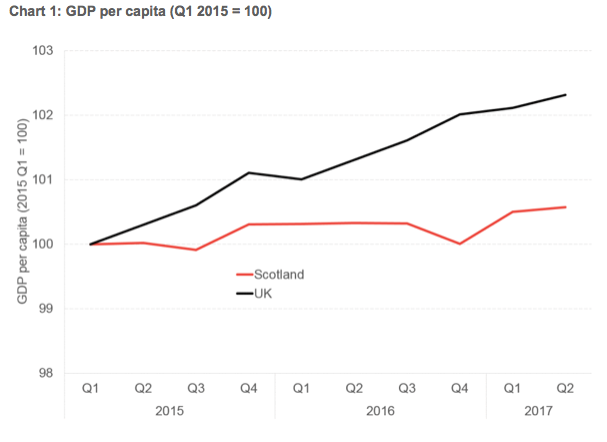

The slowdown in Scotland’s rate of economic growth relative to the UK has been well documented. Whilst growth in UK GDP per head has been weak, growing at just 2.3% between Q1 2015 and Q2 2017, Scottish growth has been weaker still, with per capita GDP growing just 0.57%, over the same period (Chart 1).

Revenues from non-savings, non-dividend (NSND) income tax now form part of the Scottish budget. Under the Fiscal Framework, the Scottish budget will be better off than it would have been without tax devolution, if revenues per capita grow more quickly in Scotland than they do in the rest of the UK (rUK). Conversely, slower growth will translate into a smaller Scottish budget.

A critical question therefore is what slower growth in GDP per capita – in Scotland relative to rUK – might mean for the growth of income tax revenues per capita in Scotland relative to rUK. Does slower growth in GDP per capita necessarily mean slower growth in income tax revenues? How strong is the relationship and what factors might influence it?

Long run relationship between GDP per capita and the income tax base

It is important to note initially that income tax revenues are a function of the tax base (the amount of taxable income), and income tax policy (allowances, rates and bands). So the first question to consider is the relationship between GDP and the tax base.

Clearly, increases in population will tend to increase both the size of economy (GDP) and the tax base (taxable income). To abstract from this relationship, let us assume that population is constant. How then might changes in GDP (i.e. GDP per capita) effect the tax base?

In the long run there must be a reasonably strong relationship between GDP per capita and the income tax base.

- GDP per capita will grow if there is an increase in employment (or hours worked) or an increase in productivity (i.e. the amount produced per hour worked).

- The income tax base will grow if hours worked or hourly wages increase.

Productivity and average wages are inextricably linked. In the long run, the only way in which average real wages can grow is through increases in productivity: productivity improvements are what enable firms to pay higher wages without increasing prices.

This link between productivity and real wages means that the two things that underpin increasing GDP per capita – hours worked and/or higher productivity – are the same two factors that can increase the size of the income tax base – hours worked and wages.

But even in the long run, the relationship between growth in GDP per capita and growth in the income tax base is unlikely to be absolutely fixed nor constant over time. This is partly because the composition of GDP growth can affect average incomes and the way in which they are distributed. For example:

- There might be changes over time in the share of labour as opposed to capital in GDP growth. In most OECD countries, the share of labour (wages and incomes) relative to capital (profits and dividends) in GDP has tended to fall in recent decades. The reasons for a falling labour share are debated, but is thought to be at least in part due to technological change, and perhaps also because of a weakening of labour’s bargaining power.

- Similarly, changes in the composition of employment between self-employment and being employed might influence the relationship between economic activity and the tax base, if self-employment is taxed differently from employment.

- The relationship between productivity and wages might also weaken over time if non-wage benefits become more important relative to wage benefits. For example, increased employer contributions to pensions or to healthcare plans or perks such as company cars might weaken the link between productivity and wage growth.

Short run relationship between GDP per capita and the income tax base

In the short run, the relationship between GDP per capita and the income tax base is likely to be weaker, for several reasons:

- There can be lags between changes in output (GDP) on the one hand and changes in employment and/or wages on the other. Firms might ‘hoard’ labour for example during an economic downturn and allow profits to fall instead. During an upswing, firms might be able to return hoarded labour to more productive uses, expanding output without needing proportionate increases in labour.

- Some factors determining the income tax base are not really affected by GDP in the short run. For example, pension income is not correlated with GDP in the short run (but in the long run of course, pension income is in large part a function of earnings during working life).

Inconsistency of geographical scales

A further complication that may weaken the relationship between growth in GDP per capita and growth of the income tax base is that the geographical level at which these things is measured is not consistent.

This is particularly the case in the Scottish context. When we talk about Scottish GDP we are usually talking about ‘onshore GDP’, i.e. we exclude activity generated by the offshore oil and gas sector in the North Sea etc. But it is quite possible that individuals working ‘offshore’ count as Scottish taxpayers for the purposes of determining Scottish income tax revenues.

More significantly, people whose main residence is in Scotland but who work partly or wholly in another part of the UK don’t directly contribute to Scottish economic output, but the income generated from this activity will form part of the Scottish income tax base (and vice versa).

Tax policy and the distribution of income

When considering the relationship between growth in GDP per capita and income tax revenues there is a further complication which may muddy the picture: the role of tax policy.

With a progressive tax system such as the UK’s, a given rate of average income growth should lead to a proportionately greater increase in revenues.

But the way in which a given level of income growth is distributed can also have a material impact. With a progressive tax system like the UK’s, wage growth that is disproportionately concentrated on those with higher incomes might strengthen the link between wages and the income tax base, whereas wage growth that is disproportionately focussed on the poor might weaken this relationship.

Summary

There must in principle be a reasonably strong correlation between growth of GDP per capita and growth of income tax revenues per capita.

But a large variety of factors mean that this relationship is likely to be much weaker in the short term. The tax base is determined not only by the wages and income of those in work, but also by income from pensions and other factors that are only weakly linked to contemporaneous economic activity. The way in which growth is shared between labour and capital, and the way in which labour income gains are distributed across the labour force also matters. Changes in tax policy can influence the size of the tax base for a given level of activity. And short term variations in economic activity might not show up immediately in wages or employment.

From this point of view, slower growth in Scottish GDP per capita without materially slower growth in income tax revenues per capita is not inconceivable as an outcome at least temporarily.

On 14 December 2017 the Scottish Fiscal Commission will publish its first ever forecasts for Scottish GDP growth and Scottish income tax revenues over the next five years. It will be interesting to see what judgement the Commission has come to about the evolution of both.

First published on Fraser of Allander Institute site

Leave a Reply